How Many Shares Do I Have?….Um…

When talking to founders, we regularly uncover confusion about share count: how much has been issued? What was that number they first put in their charter? What’s this “fully diluted” number they read about on a VC blog? As a founder, it is essential to understand your cap table, and that means knowing the difference between authorized shares, issued and outstanding shares, and fully diluted shares.

Authorized Shares. Authorized shares are the maximum number of shares a corporation is permitted to issue. This number is designated in the corporation’s Certificate/Articles of Incorporation (or “Charter”) when the corporation is formed. Authorized shares can be thought of as the total number of shares a corporation has “on the shelf” to take down and hand out plus any shares that have already been issued. If the shares stay on the shelf and are not otherwise spoken for, it’s like they don’t exist for purposes of the cap table. The number of authorized shares can typically be increased with board and stockholder approval and an amendment to the Charter.

Issued and Outstanding Shares. Issued and outstanding shares (sometimes just called outstanding shares) are those shares that have actually been sold, granted or otherwise distributed from the corporation to its stockholders. This will always be less than or equal to the number of authorized shares. Holders of issued and outstanding shares are true stockholders. Corporations typically keep a cushion of authorized but unissued shares “on the shelf” to allow for future share issuances.

Fully Diluted Shares. The term “fully diluted” is intended to capture all equity that has been issued, is spoken for or is expected to be granted. Fully diluted shares typically refer to (i) issued and outstanding shares, plus (ii) the shares the corporation is obligated to issue upon exercise or exchange of an instrument (such as stock options or warrants), and (iii) the shares reserved for issuance under an option pool. This gives stockholders a picture of what percentage of the corporation they would own after those rights are exercised.

Note: Sometimes, investors will want to understand what the share count looks like if all convertible stock or SAFEs have been converted as well; however, calculating the exact number of shares resulting from conversion of notes or SAFEs

usually requires assumptions about a subsequent financing (share price, timing, etc.), so that calculation typically only shows up in a pro forma cap table that models a subsequent financing rather than in the fully diluted calculations in a current cap table.

Founders should note that with a standard fully diluted calculation, shares are by definition overstated by a bit. An investor negotiating for a set percentage of a company on a fully diluted basis will, at the time of the initial investment, own more than the negotiated percent because of the ungranted option shares and unvested options.

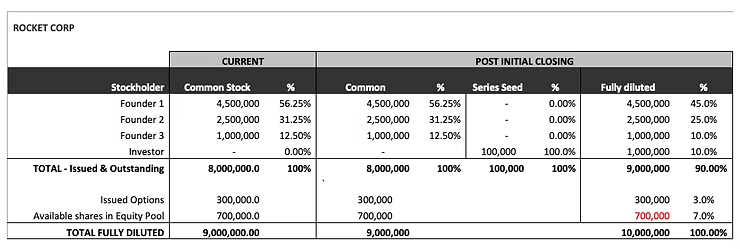

EXAMPLE:

See in the cap table below that Investor purchases 1,000,000 shares of Rocket Corp Series Seed shares for $1 per share, which constitutes 10% of the Company on a fully diluted basis. However, if the Company is sold the very next day, the 700,000 shares available under the equity plan would be disregarded (if any portion of the 300,000 issued options is not vested, those shares may be disregarded too). So while the investor negotiated for a 10% ownership stake, at closing, she actually owns at least 10.75%. This gives the investor assurances that their negotiated 10% will not be immediately reduced by an increase in the option pool immediately after investment.

It is important for stockholders to understand the difference in their percentage ownership when calculated based on issued shares as compared to fully diluted shares. Although a calculation based on issued shares provides an accurate snapshot of the current ownership structure, investors frequently rely on fully diluted shares when reviewing a company’s financial performance.